Why Halifax Home Prices Are So High

Why Halifax Home Prices Are So High And What Nova Scotia Buyers Can Actually Do About It

Published: April 2026 | Category: Market Insights | Reading Time: ~5 minutes

Halifax has earned an unwelcome distinction: one of Canada's most challenging cities for housing affordability. If you've been scrolling Reddit lately, you already know the sentiment on the ground. But the question buyers keep asking isn't just "why is it so expensive?" and it's "is there anything I can actually do about it?"

The honest answer is yes. But only if you understand what's driving prices and where the real opportunities still exist.

How Did Halifax Get Here?

Several forces collided starting in 2020. A significant wave of out-of-province buyers, many relocating from Ontario and British Columbia, arrived with equity-backed budgets far larger than the local market had ever seen. Many purchased homes sight-unseen, submitting offers $100,000 to $200,000 over asking with no conditions. That triggered a market-wide reset across Nova Scotia.

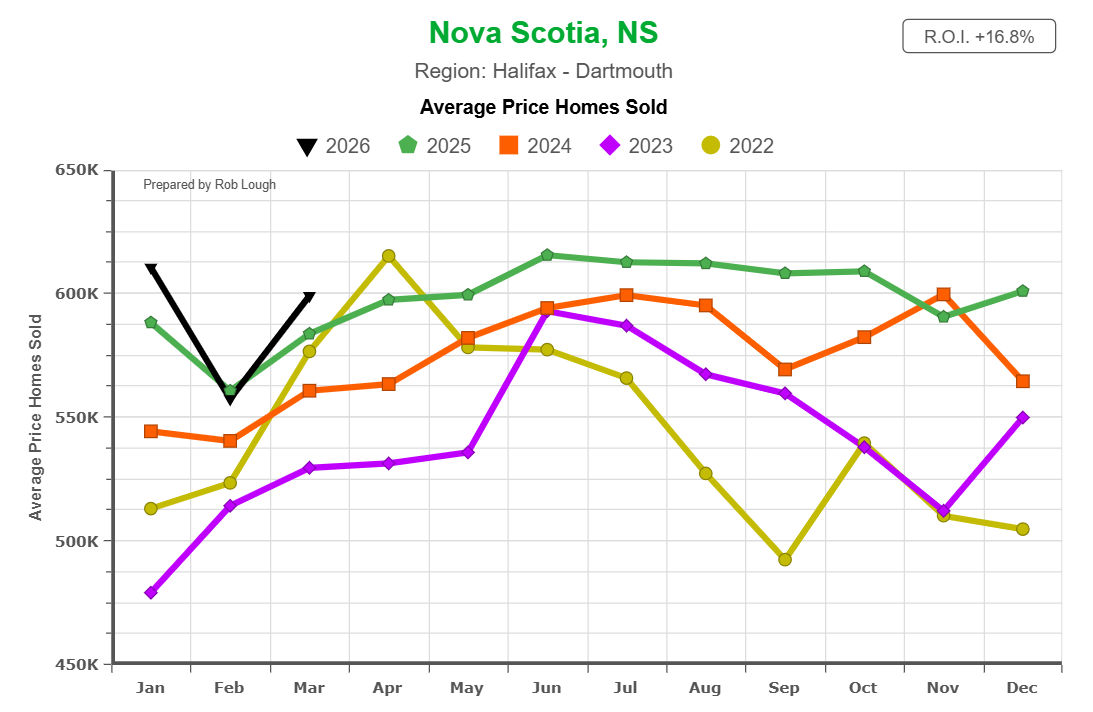

Properties that sold for $250,000 in rural Nova Scotia in 2019 are now listed near double that. The average home price in Halifax-Dartmouth reached $599,189 in January 2026, up 3.9% year-over-year. Entry-level detached homes in Halifax routinely open above $500,000.

Meanwhile, local wages have not kept pace. Halifax's living wage now stands at $28.30 per hour, and that's the floor needed for a family of four to cover basic expenses. For workers earning less, the income-to-price ratio is genuinely difficult.

Where the Market Stands in 2026

The frenzy of 2021 and 2022 has moderated. The 20-offer scenarios on every listing are behind us. In March 2026, Halifax-Dartmouth's sold-to-ask ratio sat at 98.9%, down from over 100% during peak summer conditions, meaning buyers are successfully negotiating modest discounts on the right properties.

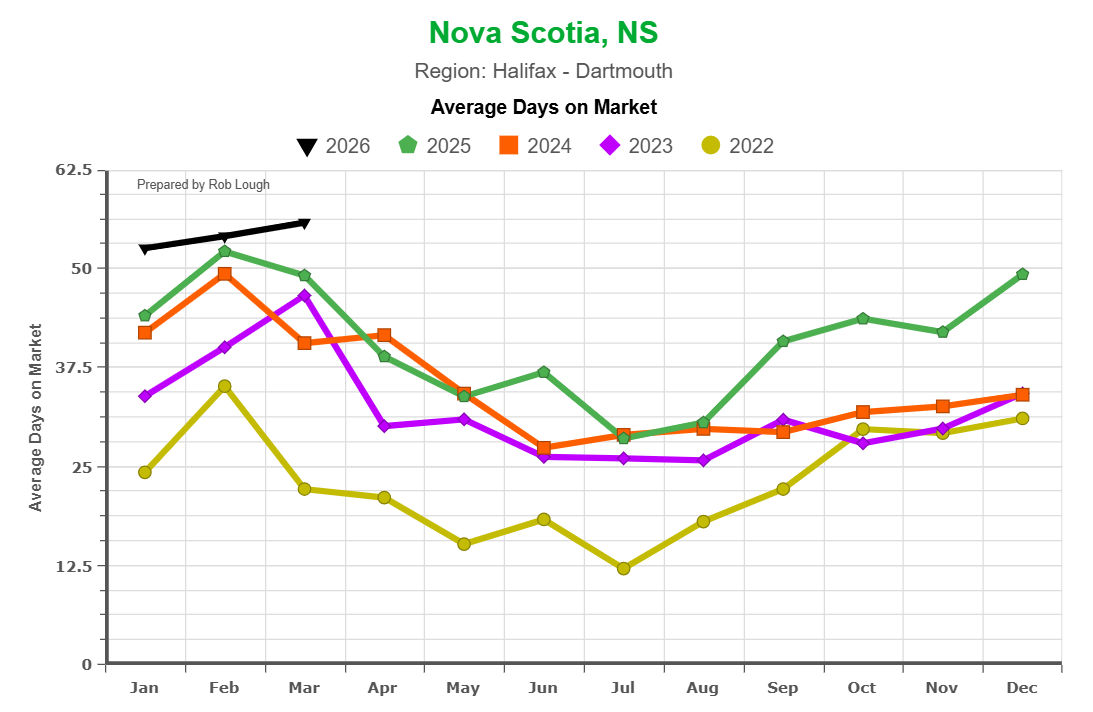

Average days on market have climbed to 52.6 days in January 2026, nearly double the pace seen at the height of summer 2025. That's not a crash. It's a more balanced market and a more balanced market creates room to act strategically.

For a deeper look at what's shaping conditions across the province, the Nova Scotia real estate market update covers the policy and supply factors at play heading into 2026.

What Nova Scotia Buyers Can Actually Do

1. Look at Dartmouth

Central Dartmouth consistently delivers better value per square foot compared to the Halifax Peninsula, with walkable neighbourhoods, waterfront parks, and ferry access to downtown Halifax. The Halifax economy overview highlights Dartmouth and Mainland Halifax as areas with the strongest multi-unit construction activity, which means more supply and more options. For buyers with a $450,000 to $600,000 budget, Dartmouth often delivers more space without sacrificing access to HRM's urban core.

2. Explore the Truro and District 104 Corridor

Truro, Bible Hill, and Stewiacke consistently come up in buyer research as an underrated market with meaningfully better pricing. The District 104 corridor is within commuting distance of HRM and offers schools, services, and infrastructure without the Halifax price premium. Our complete home buyer's guide for Nova Scotia covers Truro alongside other communities worth considering for buyers who've done their research.

3. Understand What You're Actually Paying at Closing

Sticker shock at closing catches buyers off guard. Nova Scotia closing costs typically run 2.5% to 3% of the purchase price, on a $500,000 home, that's $12,000 to $15,000 on top of your down payment. The Halifax Regional Municipality charges a Deed Transfer Tax of 1.5%, collected by your lawyer at close. Budget for it early, not at the last minute.

4. Layer the Government Programs Available to You

Nova Scotia buyers in 2026 have never had more financial assistance available, if you know where to look. The full 2026 first-time home buyer programs guide covers every program in detail, but here's the short version of what stacks together:

Nova Scotia 2% Down Payment Pilot: Nova Scotia became the first province in Canada to reduce the minimum down payment to just 2% for eligible first-time buyers purchasing through participating credit unions. The maximum purchase price in HRM and East Hants is $570,000. On a $500,000 home, this saves $15,000 in upfront cash compared to the standard 5% minimum — potentially shaving one to two years off the time it takes to enter the market.

First-Time Home Buyers' GST Rebate (Bill C-4): In force since March 2026, eligible first-time buyers can now recover the full 5% federal GST on a newly constructed home, with savings reaching up to $50,000. For a $450,000 new build in Dartmouth or HRM, that's $22,500 back. Notably, the rebate applies to agreements signed on or after March 20, 2025 — so buyers who signed last year and haven't closed may still be eligible.

RRSP Home Buyers' Plan: Withdraw up to $60,000 individually — or $120,000 combined for couples — from your RRSP tax-free toward a qualifying purchase. A two-year grace period before repayments begin reduces cash flow pressure in the years right after closing.

First Home Savings Account (FHSA): Contributions are tax-deductible going in and tax-free coming out for a qualifying home purchase. Up to $8,000 per year, $40,000 lifetime. Couples can each hold one, doubling the benefit.

First-Time Home Buyers' Tax Credit: A $10,000 non-refundable federal credit worth up to $1,500 in tax relief, claimed on your return for the year of purchase. No separate application required.

A couple who stacks FHSA savings, an HBP withdrawal, and the GST rebate on a new build can potentially access well over $200,000 in combined tax-free and rebate benefits. The 2026 first-time buyer programs guide walks through what each program requires and how they work together.

5. Consider a Property With a Suite

One underused strategy for affordability: buying a property with a legal secondary suite, or one with potential for one. Halifax allows secondary and backyard suites as-of-right in most residential zones, and government grants of up to $52,900 are available to help offset construction costs. Rental income from a legal suite can meaningfully reduce the carrying cost of a property, improving your effective affordability from day one.

6. 6. Don't Skip the Home Inspection or Treat It as a Formality

In the competitive years of 2021 and 2022, many buyers waived inspections to win offers. In 2026's more balanced market, that shortcut is far less necessary and Halifax's housing stock makes inspection skipping genuinely costly.

Halifax has some of the oldest homes in Atlantic Canada. With a coastal climate and bedrock geology that creates serious radon exposure risk, the problems that cost the most money are almost never the ones you can see on a showing. Halifax home inspection guide — what a former inspector wants every buyer to know covers what gets flagged most often in HRM and why it matters for your offer strategy.

A few Halifax-specific findings worth understanding before you buy:

Knob-and-tube wiring is present in many pre-1945 homes and most Nova Scotia insurers won't underwrite a home with active knob-and-tube — meaning no insurance, no mortgage. An inspector can detect it even where the wiring is hidden behind walls.

Radon is invisible, odourless, and a documented problem in Halifax. Health Canada testing data shows that among HRM homes built between 2012 and 2021, 67% tested above the federal guideline. Radon testing is not part of a standard inspection but any qualified inspector will recommend it. Mitigation typically costs $2,000 to $3,000 and is highly effective.

Vermiculite insulation in older attics is frequently contaminated with asbestos from the Libby, Montana processing facility. If present, it should be assumed to contain asbestos until professionally assessed.

These aren't reasons to avoid older Halifax homes — they're reasons to go in with your eyes open. With the market offering more time (52+ days average on market in January 2026), buyers can afford to do their due diligence properly. The full inspection guide walks through every system an inspector evaluates and what findings are actually deal-relevant versus normal wear on a Halifax home of a given vintage.

7. Work With a Local Agent Who Knows the Micro-Markets

The difference between a successful purchase and a costly one in HRM often comes down to hyper-local knowledge. Comparable sales matter more than list prices. Understanding which streets hold value, where supply is softening, and which neighbourhoods are seeing investment gives buyers a measurable advantage. An agent with a home inspection background brings an additional layer of due diligence to property condition and value assessment, details that matter especially when every dollar counts.

Key Takeaways for Buyers

- Average Halifax-Dartmouth sale price: $599,189 (March2026)

- Sold-to-ask ratio: 98.9% negotiation is back on the table

- Dartmouth and the Truro corridor offer the best value relative to price in HRM and beyond

- Layering government programs can meaningfully close the down payment and cash-flow gap

- Legal secondary suites can turn an affordability challenge into a manageable mortgage

The market is difficult. But buyers who understand it, and who work with a local agent who does too, are still finding paths into Nova Scotia real estate in 2026.

About the Author

Rob Lough is the Broker/Owner of Century 21 Optimum Realty, serving Halifax Regional Municipality, East Hants, and the Truro/District 104 corridor. With 25 years of Nova Scotia real estate experience, including 5 years as a licensed Home Inspector, Rob brings practical, boots-on-the-ground knowledge to every transaction. Connect with Rob.

Related Resources