First-Time Home Buyer Programs in Nova Scotia 2026 Guide

First-Time Home Buyer Programs in Nova Scotia (2026 Guide)

By Rob Lough, Broker/Owner — Century 21 Optimum Realty

Buying your first home in Nova Scotia in 2026 means navigating a landscape that has changed substantially over the past two years. New federal programs have come into effect, mortgage rules have been updated, and the Halifax-Dartmouth market continues to draw national attention. The good news: there's never been more financial assistance available to first-time buyers in this province — if you know where to look.

This guide covers every major program available to Nova Scotia first-time buyers in 2026, how they stack together, and what you need to know before you start your search.

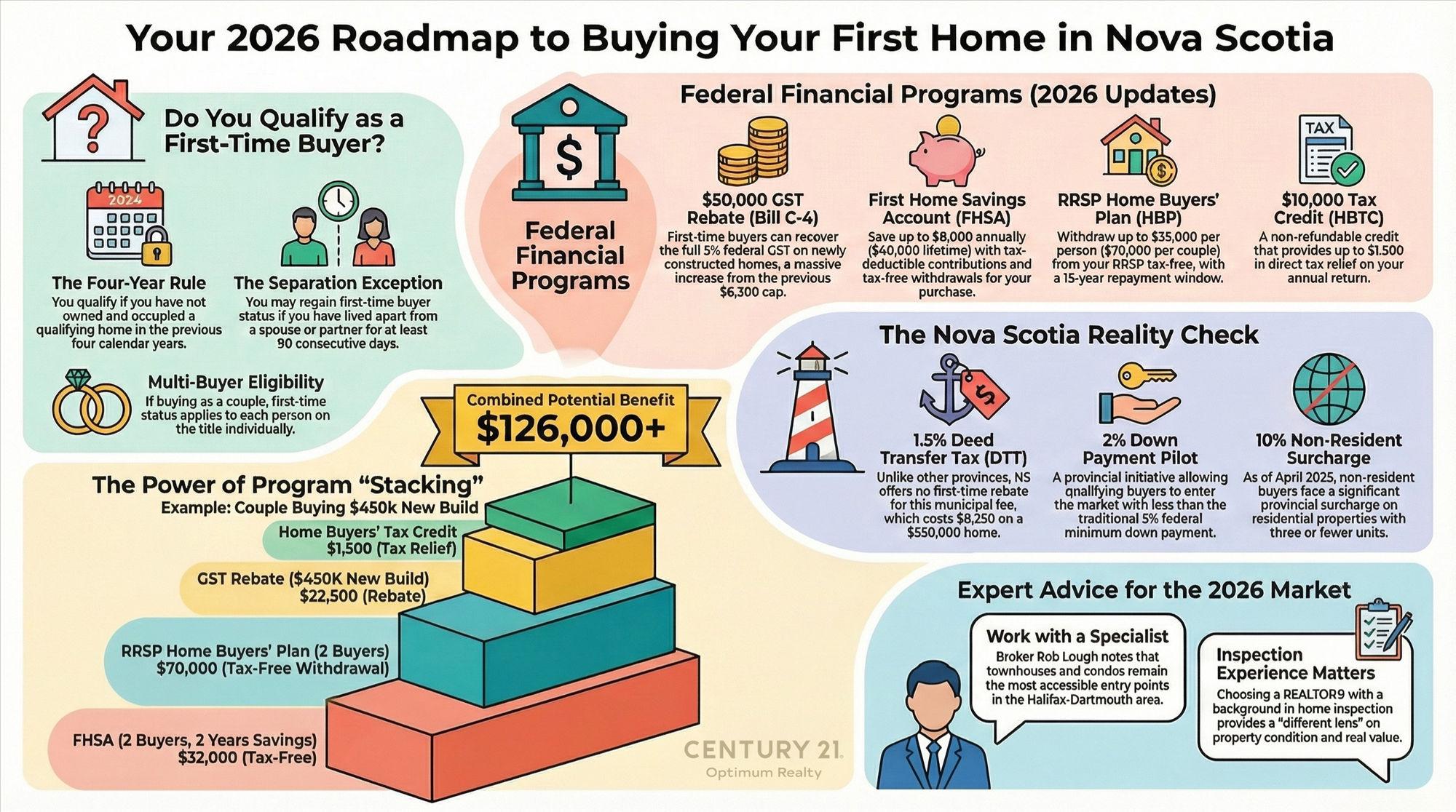

What Counts as a "First-Time Buyer" in Nova Scotia?

For most federal programs, you qualify as a first-time buyer if you have not owned and occupied a qualifying home in the previous four calendar years. This applies to each person on title, so a couple where only one partner previously owned a home may still have one qualifying buyer, depending on the program.

There's also a less-known exception for people who have separated or divorced. If you've lived apart from a former spouse or common-law partner for at least 90 consecutive days, you may regain first-time buyer status, even if you owned a home together quite recently. Read the full breakdown of first-time buyer benefits after separation for details on how this rule works in practice.

Federal Programs Available in 2026

1. First-Time Home Buyers' GST Rebate (Bill C-4)

This is the biggest development for first-time buyers in years. Bill C-4 received Royal Assent on March 12, 2026, and dramatically expanded GST relief on newly constructed homes.

Under the updated program, eligible first-time buyers can recover the full 5% federal GST paid on the purchase price of a qualifying new home, with potential savings reaching up to $50,000 on higher-priced new construction. The old rebate structure capped at $6,300 for homes under $350,000. This replaces it entirely.

One important detail for buyers mid-transaction: the rebate applies to agreements of purchase and sale entered into on or after March 20, 2025, meaning buyers who signed last year and haven't closed yet may also be eligible. If that's your situation, speak to your real estate lawyer about the retroactive claim process before closing.

For Nova Scotia buyers specifically, the math works well. Nova Scotia's 15% HST includes the 5% federal component targeted by the rebate, meaning you recover one-third of your total tax burden on a qualifying new build. On a $450,000 new home in Dartmouth or elsewhere in HRM, that's $22,500 in tax savings.

See the full GST Rebate breakdown on roblough.com for income limits, qualifying conditions, and how to apply.

2. Home Buyers' Plan (HBP) RRSP Withdrawal

The Home Buyers' Plan lets eligible first-time buyers withdraw up to $60,000 from their RRSP, tax-free, to put toward a qualifying home purchase. Couples can each withdraw up to $60,000, for a combined maximum of $120,000. This increased limit applies to withdrawals made after April 16, 2024, and replaces the previous $35,000 cap.

The federal government also extended the repayment grace period. Buyers no longer have to begin repaying the withdrawn amount immediately — there is now a two-year grace period before repayments start, which meaningfully reduces cash flow pressure in the years right after closing. After that, the amount must be repaid over 15 years. If you don't repay the required annual amount, it gets added to your taxable income for that year.

Key conditions:

- You must have a written agreement to buy or build a qualifying home

- The funds must have been in your RRSP for at least 90 days before withdrawal

- You must occupy the home as your principal residence within one year of buying or building

3. First-Time Home Buyers' Tax Credit (HBTC)

The HBTC is a non-refundable federal tax credit worth $10,000 providing up to $1,500 in tax relief at the 15% federal rate. It's claimed on your personal income tax return for the year you purchase the home.

This is one of the easiest programs to access, no application required, no separate process. Your accountant or tax preparer claims it when filing your return.

4. First Home Savings Account (FHSA)

The FHSA is a registered account that combines features of an RRSP and a TFSA specifically for first-time buyers. You can contribute up to $8,000 per year, with a lifetime limit of $40,000.

- Contributions are tax-deductible (like an RRSP)

- Withdrawals for a qualifying home purchase are tax-free (like a TFSA)

- Unused contribution room carries forward one year

- Couples can each open an FHSA, doubling the tax-free savings potential

If you haven't opened an FHSA yet, 2026 is the year to start, the sooner you open it, the more contribution room you accumulate.

Nova Scotia's 2% Down Payment Pilot

Nova Scotia made history on February 3, 2026 by becoming the first province in Canada to reduce the minimum down payment for first-time buyers to just 2% of the purchase price, less than half the standard 5% federal minimum.

The program is delivered through participating credit unions across the province (not major banks), in partnership with Atlantic Central. The Province acts as guarantor, covering 90% of any lender shortfall if a buyer defaults and the home sells for less than the outstanding mortgage balance. This structure also means no traditional CMHC mortgage default insurance is required, which is a meaningful cost saving at closing.

Key program details:

| Detail | Specifics |

|---|---|

| Minimum down payment | 2% of purchase price |

| Max purchase price (HRM + East Hants) | $570,000 |

| Max purchase price (rest of NS) | $500,000 |

| Maximum household income | $200,000 |

| Interest rate cap | Prime + 2% |

| Credit score minimum | 630 |

| Delivered by | Participating credit unions only |

| Program length | Four-year pilot |

On a $500,000 home, the difference between the standard 5% down ($25,000) and the 2% pilot down ($10,000) is $15,000 in upfront cash, potentially shaving one to two years off the time it takes a renter to save enough to enter the market.

One important trade-off to understand: a smaller down payment means a larger mortgage. Until you reach 20% equity, you're also locked into the originating credit union, you cannot switch lenders to negotiate a better rate. Plan for this if you use the program.

To apply, contact a participating credit union directly. A list of participating institutions is available at novascotia.ca/first-time-home-buyers-program-pilot.

What Nova Scotia Doesn't Offer (And What to Budget For Instead)

Unlike Ontario and British Columbia, Nova Scotia does not have a first-time buyer Land Transfer Tax rebate. What the province has instead is the Deed Transfer Tax (DTT), a one-time municipal fee due at closing.

Most municipalities in Nova Scotia, including Halifax Regional Municipality, charge the maximum rate of 1.5% of the purchase price or assessed value (whichever is higher). On a $550,000 home, that's $8,250 payable at closing and it's a cost that catches many first-time buyers off guard.

Non-resident buyers face an additional provincial surcharge of 10% as of April 1, 2025, for residential properties with three or fewer units.

Get the complete closing cost picture for Nova Scotia buyers, including DTT rates by municipality, legal fees, and what to budget for at every stage of closing.

Stacking the Programs: What a Real Scenario Looks Like

Here's a simplified example of how these programs can combine for a Nova Scotia first-time buyer couple purchasing a newly built home in 2026:

| Program | Benefit |

|---|---|

| FHSA (both buyers, full $40K each) | Up to $80,000 tax-free |

| RRSP Home Buyers' Plan (both buyers) | Up to $120,000 tax-free withdrawal |

| GST Rebate on $450K new build | $22,500 back |

| First-Time Home Buyers' Tax Credit | Up to $1,500 off taxes |

| Combined benefit | $224,000+ |

Not every buyer will access all of these simultaneously, and income limits apply to some programs. But the stacking potential is real and it's why working with an experienced agent who understands these programs matters as much as finding the right property.

What the 2026 Halifax-Dartmouth Market Means for First-Time Buyers

First-time buyers entering the HRM market in 2026 are doing so in a more balanced environment than the frenzied conditions of 2021–2022, but prices remain elevated relative to income. Townhouses and condominiums continue to offer the most accessible entry points, with condominiums particularly popular for solo buyers and couples prioritizing location over square footage.

The Complete Guide to Buying a Home in Nova Scotia walks through the full purchase process, from mortgage pre-approval to closing day, with Nova Scotia-specific context throughout. For the latest market data and analysis, visit the real estate news hub at roblough.com/news.

My Advantage as Your First-Time Buyer Agent

I've helped hundreds of first-time buyers in the Halifax-Dartmouth market navigate programs, negotiations, and the inspection process over my 25 years in Nova Scotia real estate. My background as a licensed Home Inspector for five years before becoming a REALTOR® gives me a different lens on property condition, potential problems, and real value, details that matter especially when you're buying your first home and every dollar counts.

Whether you're exploring entry-level condos in Dartmouth, a duplex in the North End, or a detached home in East Hants or the Truro corridor, I can help you find properties that work with your programs, not against them.

📞 Contact me directly to talk about your first home purchase, no pressure, just honest guidance.

Frequently Asked Questions

Can I use the FHSA and the Home Buyers' Plan together? Yes. The FHSA and HBP are separate programs and can be used in combination for the same home purchase. A couple who has maximized both could access up to $200,000 in tax-advantaged savings ($40,000 FHSA + $60,000 HBP each) toward a qualifying home. This is one of the most powerful stacking combinations available to Canadian first-time buyers.

How much is the Deed Transfer Tax in Halifax? Halifax Regional Municipality charges 1.5% of the purchase price or assessed value, whichever is higher. On a $500,000 home, that's $7,500 due at closing. There is no first-time buyer exemption or rebate on the DTT in Nova Scotia.

Can I use the Nova Scotia 2% down payment program with my FHSA or RRSP? Yes. The provincial 2% pilot reduces the minimum cash required upfront, while FHSA and HBP withdrawals can be used to fund that down payment and cover closing costs. These programs are complementary, a couple with combined FHSA savings could potentially fund the entire 2% down payment and most of their closing costs without touching other savings.

Does the GST rebate apply if I haven't closed yet but signed my agreement last year? Potentially yes. The expanded GST rebate under Bill C-4 applies to agreements of purchase and sale entered into on or after March 20, 2025. If your agreement falls within that window and you haven't closed yet, you may be able to claim the full rebate. Speak to your real estate lawyer or accountant before closing to confirm eligibility and the claim process.

What credit score do I need to qualify for a first-time buyer mortgage in Nova Scotia? For conventional insured mortgages through major lenders, most require a minimum credit score of 600–680 depending on the lender and down payment. For Nova Scotia's 2% down payment pilot through credit unions, the minimum is 630. Buyers without an established credit history may still qualify, credit unions can assess creditworthiness through alternative documentation.

Related Resources

- Your Complete Guide to Buying a Home in Nova Scotia

- Closing Costs When Buying a Home in Nova Scotia

- Canada's $50,000 GST Rebate for First-Time Buyers

- First-Time Buyer Benefits After Separation in Canada

- Latest Halifax-Dartmouth Real Estate News

Rob Lough is Broker/Owner at Century 21 Optimum Realty, serving Halifax Regional Municipality, East Hants, and the Truro/District 104 corridor. The information in this article is current as of April 2026 and is intended for general educational purposes. Program rules and eligibility conditions change — always confirm details with a licensed mortgage broker, accountant, or real estate lawyer before making financial decisions.