First-Time Home Buyer Benefits After Separation in Canada

First-Time Home Buyer Benefits After Separation in Canada: Your Complete Guide

Breaking up is hard enough. Figuring out whether you can still access first-time home buyer benefits afterward doesn't have to be.

If you've recently separated or divorced in Canada, you may be surprised to learn that several valuable federal and provincial programs are still available to you, even if you previously owned a home with your former partner. This guide breaks down what you need to know, with a particular focus on Nova Scotia buyers rebuilding their housing situation after a relationship breakdown.

What Does "First-Time Home Buyer" Actually Mean After Separation?

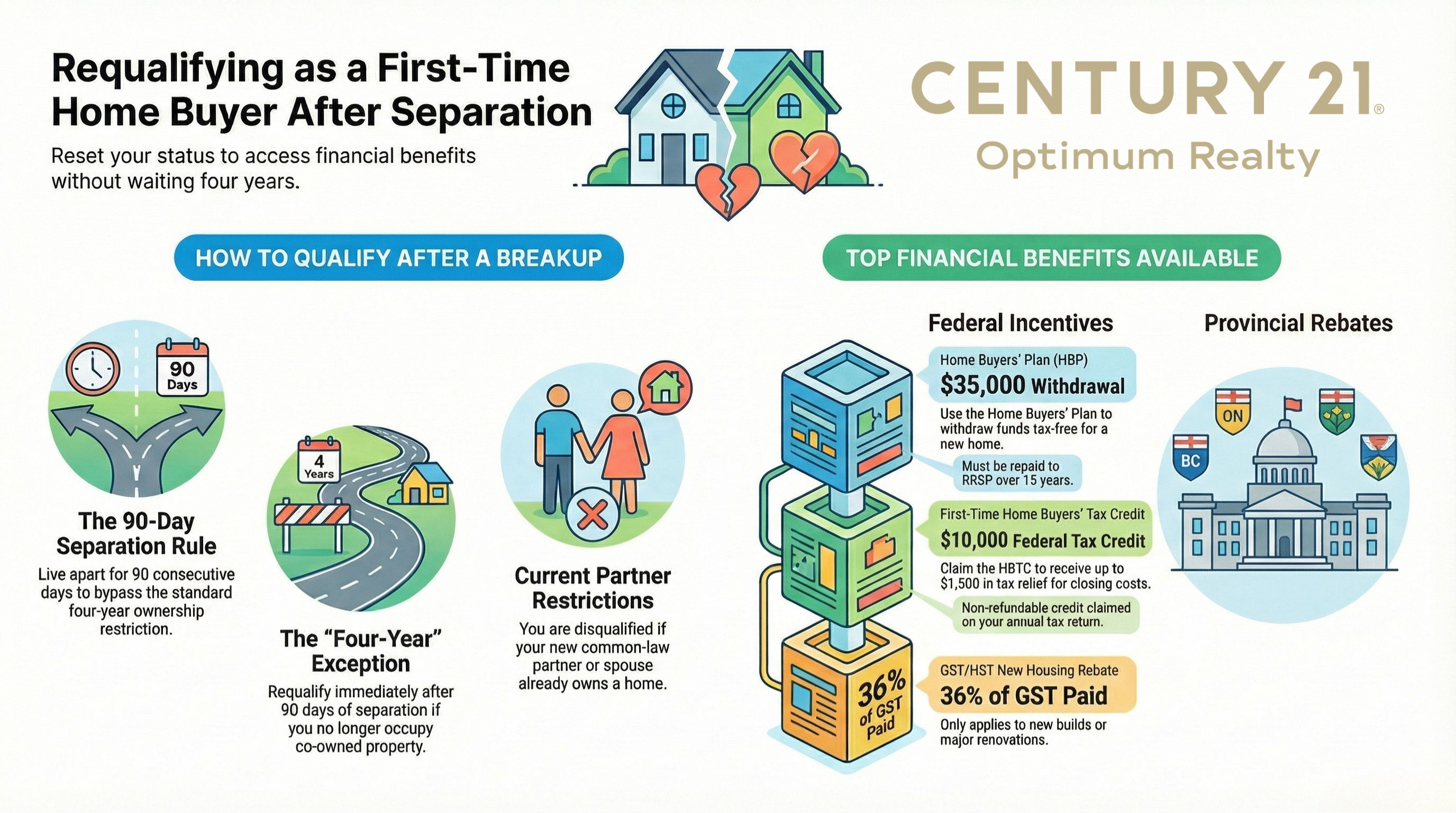

The term is misleading. In Canada, first-time buyer status isn't necessarily permanent, it can be lost and regained depending on your circumstances.

Most programs require that you have not owned and occupied a home in the previous four calendar years. However, separation creates an important exception. If you've lived apart from your former spouse or common-law partner for at least 90 consecutive days, you may requalify for first-time buyer benefits well before that four-year window closes.

This is a meaningful advantage for anyone starting over after a relationship ends.

The 90-Day Rule: Your Gateway to Requalifying

The single most important threshold to understand is the 90-day separation requirement.

You and your former spouse or common-law partner must have lived separate and apart for a minimum of 90 consecutive days before you access benefits that rely on this exception. Living apart means maintaining separate residences, not simply sleeping in different rooms of the same house.

While documentation isn't always required upfront, it's smart to keep records: utility bills or a lease agreement showing your new address, written confirmation of your separation date, and any formal separation agreement you've signed.

Once that 90-day mark passes and you're no longer occupying property you or your former partner owns, the four-year ownership clock effectively resets for program eligibility purposes.

Example: Say you and your partner owned and lived in a home together from 2020 to 2023. You separated in July 2023 and moved out. By October 2023, 90 days later, you may already qualify for first-time buyer benefits, even though you owned property just months earlier.

Home Buyers' Plan: Tax-Free RRSP Withdrawals

The Home Buyers' Plan (HBP) is a federal program that lets eligible Canadians withdraw money from their RRSP tax-free to put toward a qualifying home purchase.

After separation, you can withdraw up to $35,000 from your RRSP under the HBP. That money can go toward purchasing a new home for yourself, or in some situations, toward buying out your former partner's share in the matrimonial property.

To qualify post-separation, you must have lived apart from your former spouse or common-law partner for at least 90 consecutive days, have a written agreement in place to buy or build a qualifying home before October 1 of the year following your withdrawal, and be considered a Canadian resident at the time of withdrawal.

Keep in mind that HBP withdrawals aren't free money — they're an interest-free loan from your own retirement savings that must be repaid over 15 years. Your first repayment is typically due in the second year after withdrawal. Missed annual payments are added to your taxable income for that year, so it's worth building a repayment plan before you draw funds.

Before using the HBP, make sure your credit profile is strong. Read our guide on what constitutes a good credit score in Canada as it directly affects the mortgage terms you'll qualify for alongside any HBP funds.

GST/HST Rebate for New Construction: A Major Update for 2026

The federal government's GST rebate landscape for first-time buyers has changed significantly. Bill C-4 received Royal Assent on March 12, 2026, dramatically expanding GST relief on newly constructed homes for qualifying first-time purchasers.

Under the updated program, eligible first-time buyers can recover the full 5% federal GST paid on the purchase price of a new home — with potential savings reaching up to $50,000 on higher-priced new construction. This replaces the older, more limited rebate structure that capped out at $6,300 for homes under $350,000.

For Nova Scotia buyers, the numbers work particularly well. Nova Scotia's 15% HST includes the 5% federal component targeted by the rebate, meaning you can recover one-third of your total tax burden on a qualifying new home. On a $450,000 new build in Dartmouth or the HRM, for example, that's $22,500 in GST savings alone.

Read our detailed breakdown of the First-Time Home Buyers' GST Rebate for full program details, income limits, and how Nova Scotia buyers can maximize this benefit.

To qualify after separation, you must not have owned and occupied a home that you or your spouse owned in the previous four years, or you must meet the separation exception by having lived apart for at least 90 days and no longer occupying co-owned property.

Nova Scotia Deed Transfer Tax: No Provincial Rebate, But Know Your Costs

Unlike Ontario and British Columbia, Nova Scotia does not offer a first-time buyer land transfer tax rebate. What it does have is the Deed Transfer Tax (DTT), which most municipalities charge at 1.5% of the purchase price and it's due at closing.

On a $550,000 home, that's $8,250 in DTT you'll need to budget for. Non-residents face an additional 5% provincial surcharge on top of the municipal rate.

That said, certain transfers, including property division due to marriage breakdown, may qualify for DTT exemptions. A divorce settlement transferring the matrimonial home between former spouses is one scenario worth exploring with your real estate lawyer.

Our Nova Scotia Deed Transfer Tax guide covers current rates by municipality, exemption categories, and what to expect at closing.

First-Time Home Buyers' Tax Credit

The First-Time Home Buyers' Tax Credit (HBTC) is a non-refundable federal tax credit worth $10,000, providing up to $1,500 in tax relief at the 15% federal rate.

It's designed to offset closing costs: legal fees, disbursements, title insurance, home inspection fees, and appraisal costs. Speaking of which, if you're wondering how an appraised value differs from a real estate market valuation, our Bank Appraisal vs. CMA guide explains the difference clearly.

To qualify for the HBTC after separation, you must not have lived in a home owned by you or your spouse or common-law partner in the previous four years — or you qualify through the separation exception. The home must become your principal residence within one year of purchase. Claim the credit when filing your annual tax return.

Title Insurance: A Closing Cost Worth Budgeting For

If you're purchasing an existing home post-separation, don't overlook title insurance. For most Nova Scotia homes, owner's title insurance runs between $250 and $400 and is a one-time premium paid at closing that protects you for as long as you own the property.

Most lenders require a lender's title insurance policy as a condition of mortgage approval. Adding your own owner's policy on top is typically a modest extra cost with broad long-term protection.

Our title insurance guide for Nova Scotia buyers walks through what's covered, what's excluded, and why most homebuyers in this province consider it money well spent.

The First-Time Home Buyer Incentive: No Longer Active

The federal First-Time Home Buyer Incentive, a shared-equity mortgage program that offered 5–10% toward a down payment, was cancelled in 2024 and is no longer accepting new applicants. If you've read older articles referencing this program, it is no longer available.

Your New Relationship Could Affect Eligibility

This is a point many people miss when applying for first-time buyer benefits after separation: your current relationship status matters just as much as your past one.

If you've moved in with a new spouse or common-law partner who owns or recently owned a home, you may be disqualified from first-time buyer status, because benefit programs assess household ownership history, not just your individual history.

If you're planning to purchase with a new partner, both of you must individually meet the eligibility requirements. If your new partner owned and occupied a home within the four-year lookback period, that joint application could be affected. Plan accordingly before applying.

Understanding GDS and TDS: What Lenders Will Assess

Whether you're using the HBP, the HBTC, or any combination of programs, you still need to qualify for a mortgage. Lenders will evaluate your Gross Debt Service (GDS) and Total Debt Service (TDS) ratios to determine how much you can borrow.

After a separation, your income picture may look different, single income vs. combined, or including spousal support as qualifying income. Understanding where you stand before applying can prevent surprises.

Our guide on GDS and TDS ratios for Nova Scotia homebuyers explains how the calculations work, what lenders are looking for, and how to optimize your position before applying.

Capital Gains and the Principal Residence Exemption

When a marriage or common-law relationship ends, the transfer of the matrimonial home between former spouses can often occur on a tax-deferred basis under spousal rollover provisions. This means capital gains taxes aren't triggered at the time of transfer, giving both parties time to deal with the property without an immediate tax hit.

The principal residence exemption can also shelter capital gains from tax when the home is eventually sold. Proper designation of the matrimonial home during the separation process matters for both parties, so consulting with a tax accountant early is money well spent.

Understanding what your home is worth, through a formal appraisal versus a market-based CMA, is often the first step in structuring a fair division. Our Bank Appraisal vs. CMA guide explains the difference and when each type of valuation is appropriate.

Don't Forget Property Taxes in Your Budget

As a new homeowner, you'll be responsible for the full municipal property tax bill, not the previous owner's capped rate. In Nova Scotia, new buyers pay based on the full current market assessment, which can be significantly higher than what a long-time owner was paying on the same property.

However, if you meet the Capped Assessment Program (CAP) eligibility criteria after purchase, you can have CAP protection reinstated starting the year after your purchase, limiting future tax increases to the rate of inflation.

Our Nova Scotia Property Tax Guide covers assessments, the CAP, municipal rates, and what to expect when you buy.

Practical Steps to Access Benefits After Separation

Start by documenting your separation date clearly, that's your starting point for the 90-day requirement. Next, assess your four-year ownership history to determine whether you need the separation exception or whether the standard window has already passed.

Verify that you're not currently living in a home owned by a new partner, which would disqualify you. Gather your documentation, such as evidence of separation, proof of current residence, income verification, and RRSP contribution history if you're using the HBP.

From there, talk to a mortgage broker familiar with these programs, a real estate lawyer who can advise on property division and closing costs, and a tax accountant who can help you structure things properly. Once pre-approved, your professional team will help you claim the benefits you're entitled to at closing.

To see what's available in the current Halifax-Dartmouth market, visit our monthly market report for up-to-date pricing and inventory data.

FAQ'S

Can I use the Home Buyers' Plan if I still own part of the matrimonial home? It depends on what you're purchasing. If you've lived separately for 90+ days and are buying a different property, you may qualify. If you're buying out your former partner's share in the matrimonial home itself, special rules apply, speak with a financial advisor.

Do I need a legal separation agreement to qualify? Not necessarily. The 90-day living-apart requirement is the key threshold. A formal agreement helps document your situation clearly, but isn't always required.

What if my separation was less than 90 days ago? Wait. The full 90-day period must be complete before you can access benefits that rely on this exception.

Can my new partner and I both claim benefits if we purchase together? Both of you must individually qualify. If your new partner owned and occupied a home within the four-year lookback period, the joint application may be affected.

Final Thoughts

Separation is one of the most significant transitions a person can go through and rebuilding independent homeownership is a meaningful step forward. Canada's first-time buyer programs, combined with Nova Scotia's relatively accessible housing market, create real opportunities for people who know where to look.

The 90-day separation requirement is your gateway. You don't have to wait four full years. And with programs like the expanded Bill C-4 GST rebate for new construction, the RRSP Home Buyers' Plan, and the First-Time Home Buyers' Tax Credit available to stack, the financial assistance available to you can be substantial.

Work with qualified professionals — a mortgage broker, real estate lawyer, and tax accountant, to ensure you're accessing everything you're entitled to as you take the next step.

Ready to explore your options in the Halifax-Dartmouth market? Contact Rob Lough at Century 21 Optimum Realty. With 25 years of experience and a background as a licensed home inspector, Rob brings a uniquely comprehensive perspective to every transaction.

Related Resources

- What Is a Good Credit Score in Canada for Getting a Mortgage?

- Canada's First-Time Home Buyers' GST Rebate: What You Need to Know

- Nova Scotia Deed Transfer Tax: Complete Guide for Buyers

- TDS vs. GDS: What Nova Scotian Homebuyers Need to Know

- Title Insurance in Nova Scotia: Your Complete Guide

- Bank Appraisal vs. Real Estate CMA: What Every Homeowner Needs to Know

- Nova Scotia Property Tax Guide: Complete Overview for Homeowners

- Halifax-Dartmouth Real Estate Market Report

Disclaimer: This article provides general information about first-time home buyer benefits in Canada as of March 2026. Rules and programs are subject to change. Always consult with qualified legal, financial, and real estate professionals for advice specific to your situation.