Halifax & Atlantic Canada's Downtown Office Market

Halifax & Atlantic Canada's Downtown Office Market: A Structural Shift, Not a Blip

New research from Turner Drake & Partners confirms what many landlords and tenants already feel, the old rules of downtown office leasing across Atlantic Canada no longer apply.

By Rob Lough | Broker/Owner, Century 21 Optimum Realty | 24 Years in Nova Scotia Real Estate Published February 2026 | roblough.com

The Old Rules No Longer Apply

For more than a decade, the prevailing assumption across Atlantic Canada's commercial real estate sector was simple: office vacancies would eventually correct themselves. Rents would recover. Downtown would bounce back.

That assumption is now being directly challenged by hard data. Turner Drake & Partners' Winter 2025–2026 Atlantic Canada Newsletter, authored by the firm's economic intelligence unit, paints a clear picture of what many of us in the industry have been sensing on the ground: this is not a temporary post-COVID hangover. It is a permanent structural shift in how businesses occupy downtown office space across Halifax, Moncton, Saint John, St. John's, Fredericton, and Charlottetown.

As Turner Drake's Jigme Choerab told RENX, the finding is that there has been a structural change in demand—not a short-term cycle. The market is not recovering in the traditional sense. It is evolving into something fundamentally different.

What the Data Actually Shows

On the surface, nominal office rents across many Atlantic Canadian downtowns appear to have stabilized or even inched upward in recent years. That's the headline most people see. But Turner Drake's analysis digs deeper, and the reality beneath those headline numbers is far less comforting.

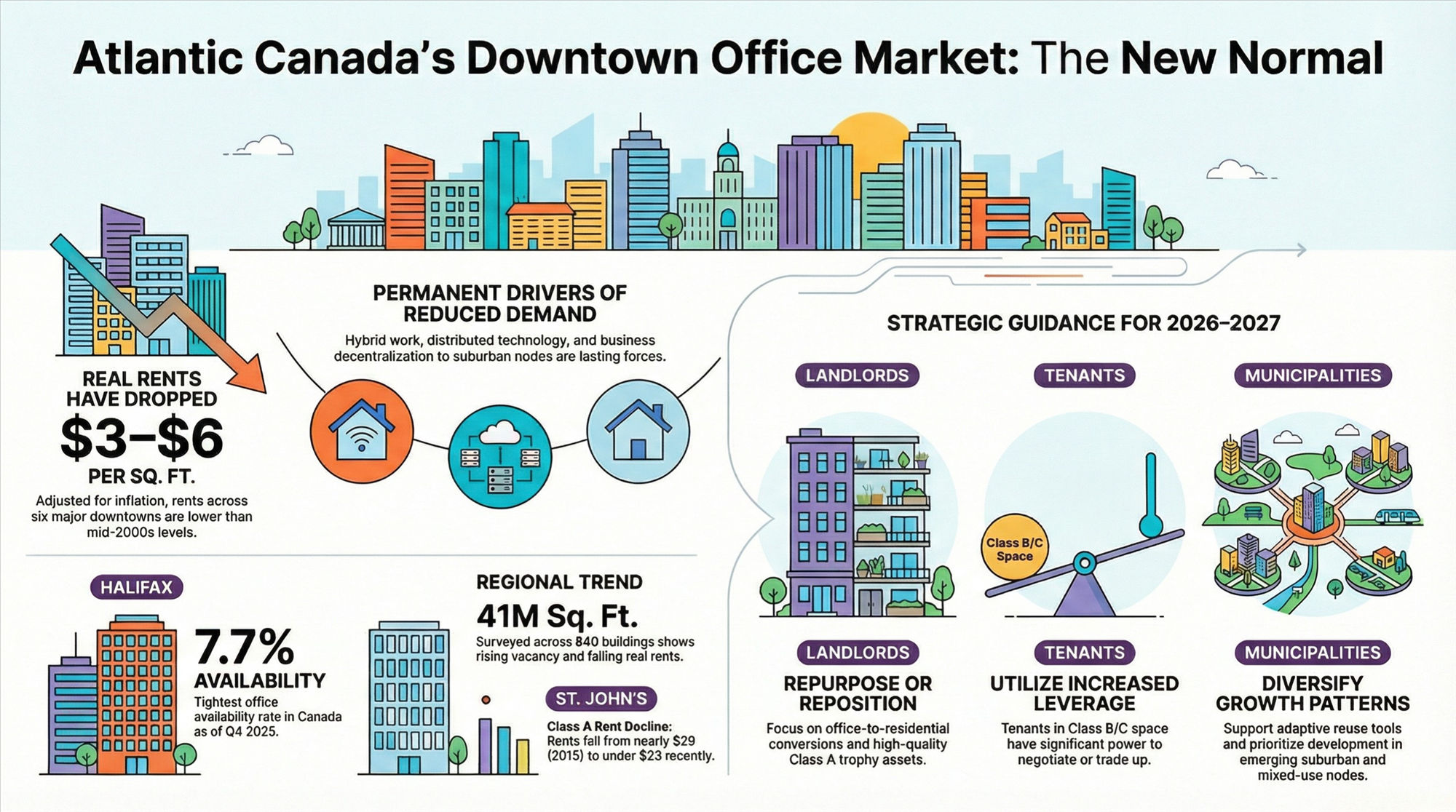

When you adjust for inflation, real rents across the region's six major downtown markets have actually declined by between $3 and $6 per square foot compared to their mid-2000s levels. At the same time, vacancy rates have been climbing steadily. The firm surveyed every single office and industrial property across Atlantic Canada, some 840 buildings totaling more than 41 million square feet, to build one of the most comprehensive datasets the region has ever seen.

The takeaway is stark: headline numbers may look steady, but once you strip out inflation and look at vacancy, the picture changes dramatically. We're seeing declining real rents and rising vacancy playing out simultaneously across every major Atlantic Canadian downtown. For context on how inflation has been affecting everyday costs across Nova Scotia, see our breakdown of The Real Cost of Living in Canada.

Why This Shift Is Happening

Several structural forces are driving this change, and none of them are temporary:

Hybrid and remote work have permanently reduced traditional office demand. The pandemic didn't create this trend—it accelerated it. Even with some return-to-office mandates gaining traction nationally (the national downtown vacancy dipped slightly in recent quarters, helped by bank and government mandates), Atlantic Canada's smaller markets haven't seen the same rebound. The hybrid model, as Turner Drake's previous research noted, is what's sustaining the office market, not reversing the decline.

Technology enables distributed work. Teams no longer need to cluster in CBD towers. Businesses of all sizes can operate effectively from suburban nodes, mixed-use locations, or fully remote setups. This is especially relevant in a region where talent is often spread across smaller communities.

Activity is decentralizing. Talent and business growth are spreading beyond historic downtown cores into suburban business parks, mixed-use corridors, and secondary markets like Dartmouth and Dieppe. Nationally, CBRE data shows suburban office assets are outperforming downtown in several regions, and Atlantic Canada is no exception. This decentralization aligns with what we've been tracking in the residential sector, too—Halifax housing starts surged 32% in 2025, with much of that construction activity happening outside the traditional downtown core.

Inventory remains stubbornly high. Unlike Calgary, which has aggressively converted office space to residential (removing over 2 million square feet in the second half of 2025 alone through its Downtown Development Incentive Program), Atlantic Canada has seen relatively limited large-scale office demolitions or conversions. This keeps supply elevated and vacancy persistent.

Halifax: A Relative Bright Spot, But Not Immune

If there's a positive story to tell in Atlantic Canada's office market, it's in Halifax. Our city has consistently outperformed other regional centres.

According to Altus Group's Q4 2025 national report, Halifax posted the tightest office availability rate in all of Canada at 7.7%—down 360 basis points year-over-year. Cushman & Wakefield's data showed the overall Halifax vacancy rate at approximately 11.5% as of Q3 2025, with positive absorption driven in part by the Dartmouth submarket. And downtown Halifax's vacancy fell to 12.4% as of early 2025, a meaningful 360-basis-point improvement year-over-year, with total downtown visits exceeding pre-pandemic levels at 19.2 million.

Several factors are working in Halifax's favour. The Canadian Urban Institute has called Halifax a "capital of conversions," noting the city punches well above its weight in office-to-residential adaptive reuse, turning obsolete office stock into much-needed housing. Nova Scotia's defence and military sector provides a stable employment anchor that other Atlantic markets lack, and the planned federal increase in defence spending could further tighten the market. The province and federal government have also committed $300 million to the Shannon Park housing project in Dartmouth, which reflects the broader trend of investment flowing into mixed-use and residential development rather than traditional office.

For a deeper look at how these trends are playing out in home values, check out our Halifax-Dartmouth Real Estate Market Statistics 2025 report.

But Halifax is not immune to the broader structural forces. The Turner Drake research applies here too: even in our strongest market, the long-term trajectory is one of selective, uneven absorption rather than broad-based recovery.

Other Atlantic Markets: Uneven Recovery

Beyond Halifax, the picture is more challenging:

St. John's continues to grapple with elevated downtown vacancy. The city had the highest office rents in Atlantic Canada but also some of the steepest declines from peak, with Class A downtown rents falling from nearly $29 per square foot in 2015 to under $23 in recent surveys. Some selective leasing and incentives have helped fill better-quality space, but the structural overhang from the oil-price construction boom lingers.

Moncton and Fredericton have maintained relatively lower vacancy rates historically, but demand softened in recent periods and real rents have trended downward. New Brunswick's markets continue to offer the lowest nominal rents in the region.

Saint John and Charlottetown round out a region where every market shares, to varying degrees, the same fundamental story: nominal rents masking real declines, and vacancy that isn't going away on its own.

What This Means for Landlords, Tenants, and Municipalities

For Landlords and Investors

Expect slower rent growth and a widening gap between top-tier downtown Class A assets and older B and C stock. The national flight-to-quality trend is real, CBRE reports that Class A properties have recorded declining vacancy in seven of ten Canadian markets, with trophy assets seeing four consecutive quarters of improvement. But that premium performance doesn't extend to commodity office space.

The smart play is repositioning or repurposing weaker buildings rather than waiting for a broad recovery that may never resemble 2010. Office-to-residential conversions, flex space configurations, and mixed-use strategies are no longer fringe ideas, they're becoming essential survival strategies. Nationally, Q4 2025 saw eight new conversion projects remove over one million square feet of office product from inventory, the largest sum for any half-year on record.

For Tenants

The structural shift gives tenants more choice and more leverage. If you're in the market for office space, especially in B and C stock, you have negotiating power that didn't exist five years ago. As Turner Drake noted, both renters and landlords need to come to terms with the real picture: nominal rents may look stable, but the actual purchasing power and market dynamics have shifted significantly in tenants' favour.

Consider trading up in quality, consolidating your footprint to a better building, or renegotiating terms on your current lease. Opportunities to lock in favourable deals in this environment are real—but they require understanding the data beneath the headlines. If you're a business owner considering a move into owned property, our article on what constitutes a good credit score for getting a mortgage in Canada is worth a read.

For Municipalities and Downtown Advocates

Office remains a critical piece of the commercial tax base. Prolonged structural weakness in office values creates fiscal pressure if assessments soften over time and in a region where downtown vibrancy depends on daytime foot traffic, the ripple effects touch retail, restaurants, and transit. For a closer look at how commercial and residential property taxes interact in HRM, see our analysis of how Halifax property taxes compare to other Canadian cities.

As Choerab advised, city planners should consider reorienting their thinking and not exclusively focusing on downtown cores. Growth should be more diversified across the areas of the municipality. Economic development strategies that focus only on downtown trophy offices risk missing emerging suburban nodes and mixed-use corridors where activity is actually growing.

Halifax's approach of incentivizing office-to-residential conversions through its Housing Accelerator Fund is exactly the kind of adaptive policy response other Atlantic municipalities should study.

Looking Ahead: Practical Guidance for 2026–2027

For investors: Focus on quality, location, building specs, and tenant profile. Target assets with a clear path to repositioning or conversion rather than betting on a broad rent rebound. The data is clear that absorption will be selective and uneven by asset class, submarket, and building quality. The broader Canadian housing market is showing early signs of buyer activity heading into 2026, which may further support conversion economics.

For business owners: Re-evaluate your space needs with hybrid work firmly in mind. Ask whether downtown still aligns with your workforce and client base, or whether a suburban or mixed-use location might serve you better. The leverage is yours right now, use it.

For policymakers: Plan for a more diversified pattern of growth. Support adaptive reuse tools that can right-size aging office inventories while addressing the housing shortage. The most successful municipal responses, from Calgary's conversion program to Halifax's emerging incentive framework, treat the office surplus as an opportunity rather than simply a problem.

"Recent economic intelligence on Atlantic Canada's downtown offices suggests we're not waiting for a 'return to normal.' We're already living in a new normal—where demand, pricing power, and risk are permanently reshaped by hybrid work, technology, and shifting urban growth patterns."

Related Resources

- Halifax-Dartmouth Real Estate Market Statistics 2025

- Truro Real Estate Market Report 2025

- Nova Scotia and Ottawa Partner on $300M Shannon Park Housing Project

- Halifax Housing Starts Surge 32% in 2025

- How Halifax Property Taxes Compare to Other Canadian Cities

- The Real Cost of Living in Canada

- Canadian Housing Market Shows Early Signs of Buyer Activity Heading Into 2026

- Re/Max Predicts Modest Home Sales Recovery in 2026 Amid Growing Inventory

Rob Lough is a Broker/Owner and Realtor® at Century 21 Optimum Realty, with 25 years of experience in Nova Scotia real estate. He serves the Halifax Regional Municipality, East Hants, and Truro markets. For real estate advice, market insights, or to discuss your property goals, visit roblough.com or contact Rob directly.

Disclaimer: This article is for informational purposes only and does not constitute financial, investment, or legal advice. Market data cited is sourced from Turner Drake & Partners, CBRE, Cushman & Wakefield, Altus Group, and other publicly available industry reports. Always consult qualified professionals before making investment or real estate decisions.