Canada's Average Rent Falls for the 19th Straight Month What It Means for Nova Scotia

Canada's Average Rent Falls for the 19th Straight Month: What It Means for Nova Scotia

By Rob Lough, Broker/Owner | Century 21 Optimum Realty

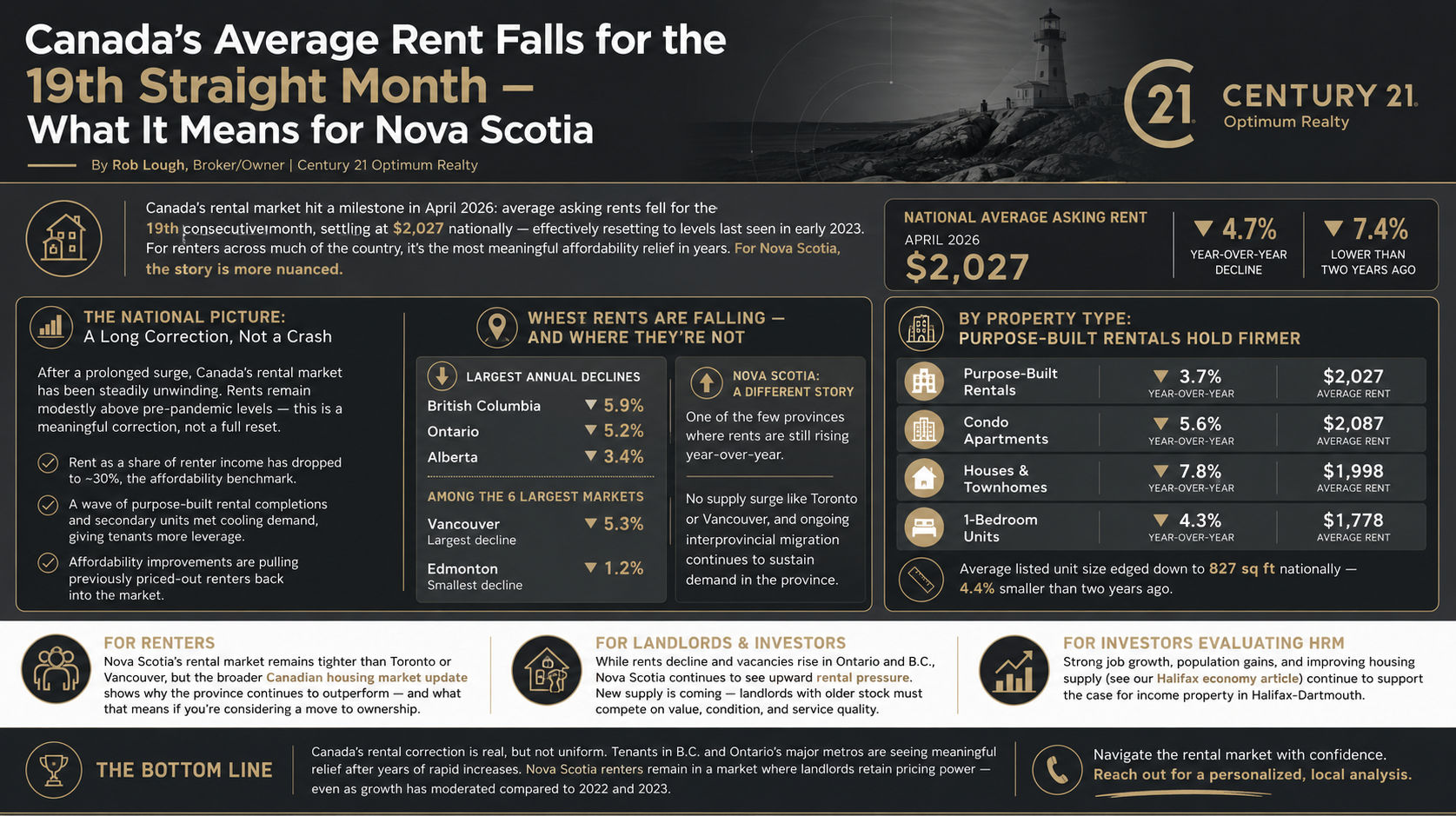

Canada's rental market hit a notable milestone in April 2026: average asking rents fell for the 19th consecutive month, settling at $2,027 nationally, effectively resetting to levels last seen in early 2023. For renters across much of the country, it represents the most meaningful affordability relief in years. For Nova Scotia, the story is more nuanced.

The National Picture: A Long Correction, Not a Crash

After a prolonged surge earlier in the decade, Canada's rental market has been steadily unwinding. The April 2026 figure of $2,027 represents a 4.7% year-over-year decline and sits roughly 7.4% below where rents were two years ago. That said, rents remain modestly above pre-pandemic levels, this is a meaningful correction, not a full reset.

Urbanation president Shaun Hildebrand has described the shift as an improvement in affordability capable of pulling previously priced-out renters back into the market. Nationally, rent as a share of renter income has dropped to approximately the 30% affordability benchmark for the first time in several years, a combination of falling asking rents and modest wage growth.

The primary driver is supply. A wave of purpose-built rental completions and secondary market units hit the market just as population-driven demand cooled, creating an unusual period of tenant leverage in many cities. We covered the early stages of this national supply push in our Halifax housing starts analysis, which shows how Halifax's construction boom has played out differently than other major centres.

Where Rents Are Falling and Where They're Not

The largest annual declines are concentrated in the high-priced provinces that led the run-up: British Columbia is down 5.9%, Ontario is down 5.2%, and Alberta has declined 3.4%. Among the six largest rental markets, Vancouver led with a 5.3% year-over-year drop while Edmonton saw the smallest decline at 1.2%. Suburban markets around major metros are seeing some of the sharpest corrections, with double-digit drops in places like Markham, Oakville, Coquitlam, and Burnaby.

Nova Scotia is a different story. The province is one of only a handful where rents are still rising on an annual basis. That's consistent with what we documented in our earlier piece on Canada's rental affordability trends, where Nova Scotia and Halifax were already standing apart from the national cooling trend. The province hasn't experienced the supply surge pressuring rents in Toronto and Vancouver, and ongoing population growth through interprovincial migration continues to sustain demand.

By Property Type: Purpose-Built Rentals Hold Firmer

Not all rental segments are behaving the same way nationally:

- Purpose-built rentals saw the smallest decline, down 3.7% year-over-year to an average of $2,027. Professionally managed apartment buildings are proving more resilient than investor-owned condos.

- Condo apartments fell 5.6% to $2,087, as investor-landlords face growing pressure to fill units in softening markets.

- Houses and townhomes dropped 7.8% to approximately $1,998 the sharpest correction of any property type.

- One-bedroom units led declines by bedroom count, falling 4.3% to $1,778 nationally.

Average listed unit size also edged down to 827 square feet nationally, a continuation of a multi-year trend toward smaller rental product, with average units now 4.4% smaller than two years ago.

What This Means for Renters and Landlords in Nova Scotia

For renters: If you've been priced out of homeownership and wondering whether to keep renting or make a move, the current market is worth a close look. Nova Scotia's rental market remains tighter than what's happening in Toronto or Vancouver, but the broader Canadian housing market update outlines why the province continues to outperform and what that means for buyers who decide the time is right to transition into ownership.

For landlords and investors: Nova Scotia's relative strength in the national context is meaningful. While landlords in Ontario and B.C. are watching rents decline and vacancies rise, this province continues to see upward rental pressure. That said, tenant expectations are rising alongside the quality of new product entering the market. The Halifax suburban housing accelerator plan will bring thousands of new units online over the coming years, landlords with older stock will need to compete on value, condition, and service quality.

For investors evaluating HRM: The Halifax economy article covers the fundamentals in detail, job creation, population growth, and improving housing supply and reinforces why this market continues to attract investment even as much of Canada cools. Strong employment, constrained resale inventory, and an active rental base continue to support the case for income property in Halifax-Dartmouth.

The Bottom Line

Canada's rental correction is real, but it is not uniform. Tenants in B.C. and Ontario's major metros are finally seeing meaningful price relief after years of rapid increases. Nova Scotia renters, by contrast, remain in a market where landlords have retained some pricing power, even as the pace of growth has moderated compared to 2022 and 2023.

For anyone navigating the rental market, the buy-vs-rent calculation, or rental property investment in Halifax-Dartmouth or across HRM, the landscape has shifted enough that a current, localized analysis matters more than national headlines. Reach out directly to talk through what the numbers look like for your specific situation.

Related Resources

- Canada's Rental Market Posts Record Decline (Dec 2025)

- Canada's Rental Affordability Crisis Deepens in 2025

- Halifax Housing Starts: A Detailed Market Analysis

- Halifax Economy 2025

- Halifax Short-Term Rental Guide 2025

Data sourced from Rentals.ca and Urbanation's National Rent Report, April 2026.