Scotiabank Predicts Bank of Canada Rate Hike in 2026

Scotiabank Predicts Bank of Canada Rate Hike in 2026 – Breaking From Market Consensus

The Bank of Canada's monetary policy direction has become a hot topic for Canadian homebuyers, mortgage holders, and real estate professionals. While most major financial institutions expect interest rates to remain stable throughout 2026, Scotiabank has broken ranks with a contrarian forecast that could significantly impact the housing market and mortgage strategies in Nova Scotia and across Canada.

Scotiabank's Contrarian Forecast

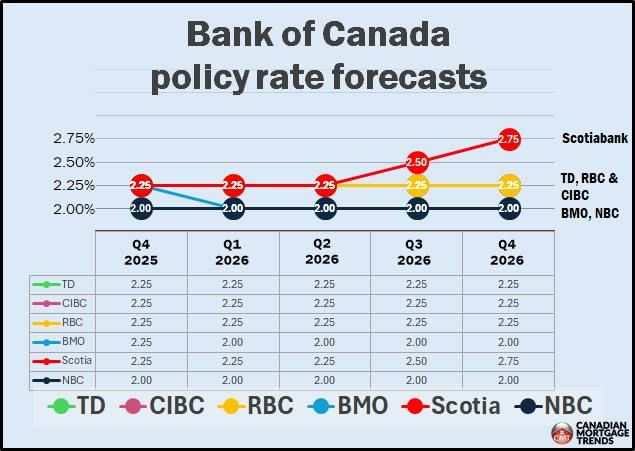

Scotiabank economists are predicting that the Bank of Canada's next significant monetary policy move will be an interest rate hike, expected in the second half of 2026. This stands in stark contrast to the broader market consensus, which anticipates the overnight rate will hold steady at or near 2.25% through most of 2026.

This divergent view comes after the Bank of Canada executed a series of rate cuts throughout 2025, bringing the overnight rate down from its peak of 5% to 2.25% by October. According to Scotiabank, this rate-cutting cycle has concluded, and economic conditions will warrant a reversal by late 2026.

What Other Major Banks Are Predicting

The majority of Canada's largest financial institutions including TD Bank, RBC, and CIBC maintain a more conservative outlook:

- Policy rate stability: Most analysts expect the overnight rate to remain at 2.25% for most of 2026 or potentially longer

- No immediate increases: The consensus view suggests no major rate hikes are on the immediate horizon

- Cautious approach: These forecasts align with the Bank of Canada's stated commitment to careful monetary policy as the economy adjusts to previous cuts

This makes Scotiabank's prediction particularly noteworthy, as it suggests a fundamentally different economic trajectory than what most market participants are preparing for.

Economic Factors Driving Scotiabank's Outlook

Scotiabank's contrarian position isn't based on speculation. It's rooted in several key economic factors:

Growth and Inflation Dynamics

Scotiabank economists point to expectations of improving economic growth combined with persistent inflation as primary drivers for future rate increases. While the Bank of Canada projects inflation to hover around 2% in the medium term, Scotiabank suggests inflation may prove stickier than anticipated, potentially requiring tighter monetary policy.

Trade and Economic Adjustment

The forecast also considers the lingering effects of trade tensions and economic adjustments following US-Canada tariff disputes. These factors could influence both growth trajectories and inflationary pressures in ways that necessitate policy responses.

Labour Market and Economic Indicators

Current economic conditions show improved labour market data and moderating headline inflation. While these conditions have made further rate cuts less likely in the near term, Scotiabank believes they could set the stage for rate increases if growth accelerates beyond expectations.

What This Means for Nova Scotia Homebuyers and Mortgage Holders

The divergence in forecasts creates both challenges and opportunities for those navigating the Halifax real estate market and broader Nova Scotia housing landscape:

For Variable Rate Mortgage Holders

With variable rates currently at multi-year lows following the 2025 rate cuts, borrowers enjoying today's reduced payments should consider:

- The potential for rates to begin climbing again by late 2026

- Whether locking in current rates through conversion to fixed mortgages makes sense for their situation

- Budget planning for potential payment increases 18 to 24 months from now

For Fixed Rate Shoppers

Fixed mortgage rates remain influenced by bond markets and global economic conditions rather than the overnight rate directly. However:

- If Scotiabank's forecast proves accurate, today's fixed rates may look attractive in hindsight

- The spread between variable and fixed rates will be an important consideration for those choosing mortgage products

- Long-term fixed rates (5 year terms) may offer more stability if rate hikes materialize in 2026

For First-Time Buyers and Those Planning to Purchase

Understanding the rate environment helps with timing and affordability calculations:

- If rates remain stable through 2026 as most banks predict, affordability conditions may improve gradually as incomes rise

- If Scotiabank is correct and rates increase, buyers who purchase before late 2026 with variable rates may face higher carrying costs

- Stress test requirements already factor in rate increases, so qualified buyers today should be able to handle modest increases

The Broader Economic Picture

The Bank of Canada has resumed providing detailed economic forecasts, projecting GDP growth to improve slowly over the coming years. Key considerations include:

- Policy caution: The central bank has emphasized a measured approach to monetary policy

- Economic digestion: The economy needs time to adjust to the significant rate cuts already implemented

- Global uncertainties: International economic conditions and trade relationships continue to influence Canadian policy decisions

Most institutions are now calling this the end of the rate-cut cycle, barring major new economic shocks. The question becomes whether the next move is up (as Scotiabank predicts) or an extended period of stability (as others forecast).

Strategic Considerations for Real Estate Professionals

For realtors serving clients in Halifax, Dartmouth, and throughout the Halifax Regional Municipality, this forecast divergence creates important conversation points:

- Client education: Helping buyers and sellers understand how different rate scenarios might affect their decisions

- Mortgage pre-approvals: Encouraging buyers to get pre-approved quickly to lock in current qualification criteria

- Timing strategies: Discussing whether clients' situations favor acting now versus waiting

- Market positioning: Understanding how rate expectations influence buyer psychology and market activity

The Bottom Line

While Scotiabank stands alone among major Canadian banks in forecasting a rate hike by late 2026, their analysis is based on legitimate economic factors that bear watching. Whether their contrarian view proves accurate or the consensus forecast of stable rates prevails, the outcome will significantly impact Canadian borrowers, the mortgage market, and real estate activity.

For Nova Scotia homebuyers and mortgage holders, the key takeaway is to remain informed and flexible. Variable rate holders should budget conservatively and understand their conversion options. Those shopping for mortgages should carefully weigh the trade-offs between variable and fixed rates based on their risk tolerance and financial circumstances.

As we move through 2025 and into 2026, monitoring economic indicators including inflation trends, GDP growth, and labour market conditions will provide clues about which forecast proves more accurate. In the meantime, working with knowledgeable real estate and mortgage professionals can help you navigate these uncertainties and make informed decisions for your unique situation.

Looking for expert guidance on buying, selling, or investing in Nova Scotia real estate? Contact Rob at Century 21 Optimum Realty to discuss how current and future interest rate environments might affect your real estate plans.