Bank Appraisal vs. Real Estate CMA What Every Nova Scotia Homeowner Needs to Know

Bank Appraisal vs. Real Estate CMA: What Every Nova Scotia Homeowner Needs to Know

By Rob Lough, Broker/Owner Century 21 Optimum Realty Updated: March 2026

Whether you're buying your first home in Dartmouth, refinancing in Bedford, or preparing to list in Truro, you'll likely encounter two different property valuation tools: a bank appraisal and a real estate CMA (Comparative Market Analysis). Both tell you what a property could be worth, but they serve very different purposes, and confusing the two can lead to costly surprises.

Here's what every homeowner and buyer in Halifax Regional Municipality, East Hants, and the greater Nova Scotia market needs to understand.

What Is a Bank Appraisal?

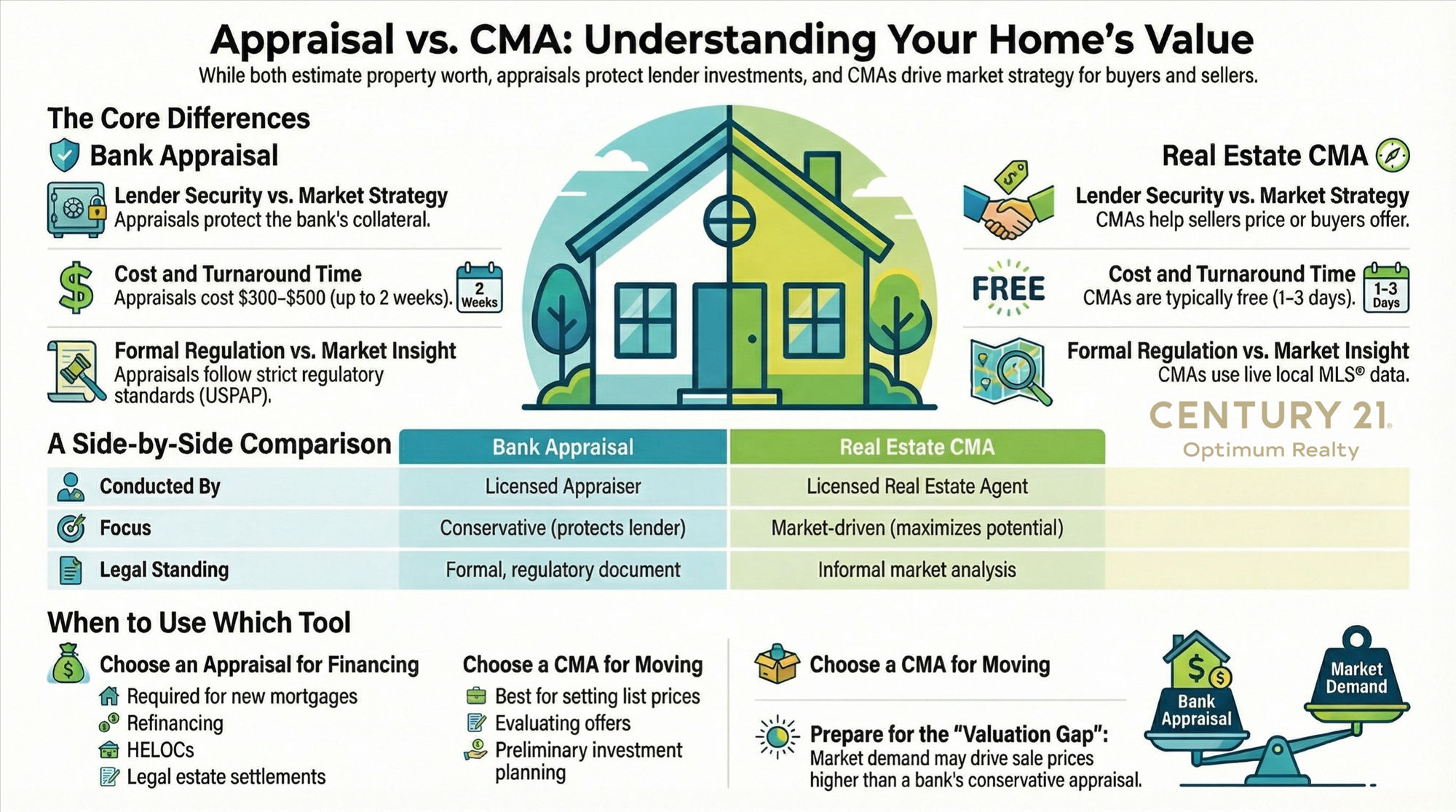

A bank appraisal is a formal property valuation ordered by your mortgage lender and conducted by a licensed or accredited appraiser. Its primary purpose is to protect the lender, not you! The bank needs to confirm that the property serves as adequate security for the amount they're lending before they'll advance funds.

Appraisers complete the process through an in-person inspection of the property, reviewing its condition, size, layout, location, and any renovations or improvements. They then pull recent comparable sales to arrive at a fair market value.

The result is a formal written report that meets regulatory standards and can be used for legal and lending purposes. Bank appraisals must follow the Uniform Standards of Professional Appraisal Practice (USPAP), which govern methodology and documentation requirements.

When Is a Bank Appraisal Required?

- Applying for a new mortgage or purchase financing

- Refinancing your existing mortgage

- Accessing a home equity line of credit (HELOC)

- Estate settlement or inheritance matters

- Appealing your Nova Scotia property tax assessment

- Legal disputes involving property value

Appraisals typically cost $300–$500 in Nova Scotia and are almost always paid by the buyer or borrower. They take anywhere from a few days to two weeks to complete.

What Is a Real Estate CMA?

A Comparative Market Analysis (CMA) is a property valuation prepared by a licensed real estate agent using current MLS® data and local market knowledge. Unlike a bank appraisal, a CMA is market-focused, its goal is to help sellers price their home competitively, or to help buyers understand the fair value of a property they're considering.

CMAs are typically provided free of charge as part of the listing consultation process. If you're thinking about selling your home and want to know what it's worth in today's market, a free home evaluation is the place to start.

A strong CMA considers:

- Recent comparable sales (typically within the last 60–90 days)

- Active competition in your price range

- Current buyer demand and inventory levels

- Property-specific strengths and weaknesses

- Neighbourhood trends and seasonal timing

Because CMAs draw on live MLS® data and a Realtor®'s firsthand knowledge of the market, they can respond quickly to shifts in conditions — something a formal appraisal, which follows a stricter point-in-time methodology, cannot always do.

For context on what the Halifax-Dartmouth market is doing right now, our monthly market reports are updated regularly with the latest sales data, price trends, and inventory stats.

Bank Appraisal vs. CMA: Key Differences

| Bank Appraisal | Real Estate CMA | |

|---|---|---|

| Conducted by | Licensed appraiser (selected by lender) | Licensed real estate agent |

| Primary purpose | Mortgage approval / lender risk protection | Listing price strategy / market insight |

| Legal standing | Formal, regulatory-compliant document | Informal market analysis |

| Cost | $300–$500 (paid by borrower) | Free |

| Turnaround | Several days to 2 weeks | 1–3 days |

| Focus | Conservative, protects lender's collateral | Market-driven, maximizes sale potential |

| Best used for | Financing, refinancing, legal/tax matters | Listing, offer evaluation, investment planning |

The Conservative vs. Optimistic Gap

One of the most important things to understand: bank appraisals and CMAs can produce different numbers for the same property and both can be "correct."

Lenders need appraisers to be conservative. If a borrower defaults, the bank must be confident it can recover the loan through a forced sale. Appraisers therefore tend to weight recent comparable sales carefully and apply stricter adjustments.

CMAs, by contrast, reflect what the market is actually doing right now, including buyer demand, competition levels, and the emotional factors that influence real-world sale prices. In a competitive Halifax-Dartmouth seller's market, a well-prepared CMA may produce a higher value than a formal appraisal, simply because it captures dynamics that formal appraisal methodology isn't designed to reflect.

This gap is important to understand when you're buying. If you offer above asking price and the bank's appraiser comes in below your purchase price, you may be responsible for covering the difference out of pocket, on top of your closing costs in Nova Scotia. That's a scenario worth planning for in advance.

Which One Do You Need?

You need a Bank Appraisal when:

- Applying for a mortgage or refinancing

- Taking out a HELOC or equity loan

- Settling an estate or navigating a divorce involving property

- Appealing a property tax assessment

- Needing a legally defensible value for any purpose

You need a CMA when:

- Preparing to list your home for sale

- Evaluating whether an offer price makes sense

- Deciding whether now is the right time to sell

- Considering a refinance and want a preliminary estimate first

- Analyzing investment opportunities in your area

If you're a buyer and want to understand the full financial picture, mortgage pre-approval, closing costs, land transfer taxes, and what lenders actually look at, our Nova Scotia Buyers Guide covers all of it in one place.

Tips for Sellers: Getting the Most From Your CMA

Interview more than one agent. The quality of a CMA depends on the agent's knowledge of your specific neighbourhood, not just access to MLS® data.

Ask for the reasoning. A good CMA explains why comps were chosen — not just what they sold for.

Think about timing. CMAs reflect current conditions. A CMA prepared in January may tell a different story than one prepared in May, particularly in Halifax-Dartmouth where seasonal patterns are pronounced.

Don't confuse list price with value. A good Realtor® will tell you what the market will bear, not just what you want to hear.

Tips for Buyers: Preparing for the Appraisal Process

Have your finances in order. Appraisals are triggered by mortgage applications, so mortgage pre-approval should come first.

Understand your credit standing. Lenders use your credit score alongside the appraisal to determine your mortgage terms. If your score needs work, it's worth reviewing our guide to credit scores and mortgage qualification in Canada before you start house hunting.

Budget for the gap. If you're buying in a competitive market and offering over asking, discuss with your mortgage professional what happens if the appraisal comes in below purchase price.

Don't make large financial changes before closing. Between approval and closing, any new debt or credit application can affect your mortgage. See: Why You Shouldn't Finance Anything Before Closing Day.

The Bottom Line

Bank appraisals and real estate CMAs are both legitimate, useful tools — but they answer different questions. An appraisal tells your lender what the property is worth as collateral. A CMA tells you what it's worth right now, in the real world, to real buyers.

Understanding the difference helps you plan your purchase or sale more effectively, avoid costly surprises, and walk into any transaction with confidence.

Have questions about where your home fits in today's Halifax-Dartmouth or Nova Scotia market? Contact Rob Lough at Century 21 Optimum Realty for a no-obligation home evaluation or buyer consultation.

Related Resources