MLI Select Program Canada Complete Guide to CMHC Multi-Unit Financing in 2026

MLI Select Program Canada: Complete Guide to CMHC Multi-Unit Financing in 2025

Posted by Rob Lough, Broker/Owner, Century 21 Optimum Realty

Canada's housing affordability crisis has driven some of the most ambitious financing policy changes in a generation, and the MLI Select program stands near the top of that list. For real estate investors and developers looking to build or acquire multi-unit rental properties, this CMHC initiative offers financing terms that are genuinely difficult to match anywhere else in the market.

This guide covers everything you need to know about the MLI Select program in 2025, including updated benefit tiers, the revised premium framework, accessibility standards, and what the program looks like for projects right here in Atlantic Canada.

If you want context on why development financing is surging across Canada right now, read this first: Canadian Bank Loans for Real Estate Development Are Surging -- Here's What's Behind the Boom

What Is the MLI Select Program?

The MLI Select program is a CMHC-backed mortgage loan insurance product designed specifically for multi-unit residential rental properties. It rewards developers and investors who commit to creating housing that is affordable, energy-efficient, or accessible, with better financing terms in direct proportion to the depth of those commitments.

Rather than offering a flat set of terms, the program uses a points-based scoring system. The more points your project earns, the better the loan-to-value ratio, amortization period, and insurance premium discount you can access.

The result is a program that genuinely aligns private sector investment with public housing goals, and creates real financial upside for investors willing to structure their projects accordingly.

MLI Select is one of several CMHC-backed tools available to developers in Canada right now. If your project is at the construction financing stage and you want to compare options, the [NEW LINK] Apartment Construction Loan Program (ACLP) is worth understanding alongside MLI Select, as the two programs serve different phases of a project's lifecycle.

What's New in 2024 and 2025: Key Program Updates

Before diving into the full details, here is a quick summary of the most significant changes since mid-2024. If you read an older guide, this section matters.

Amortization extended in specific scenarios. The standard maximum amortization under MLI Select remains up to 50 years. In certain limited circumstances, primarily tied to default management or at-risk projects, CMHC has extended this to 55 years. This is not a default option available to all applicants. Most new construction will still underwrite in the 40 to 50 year range.

Affordability is now the anchor for top-tier benefits. Since June 2024 rule revisions, projects generally need to combine categories to reach 100 points. Affordability has become the primary pathway to maximum benefits. Energy efficiency and accessibility typically need to be layered on top of an affordability commitment to reach 100 points, not used as a standalone route.

Updated accessibility standards. CMHC now explicitly references CSA B651:23 and Rick Hansen Foundation Accessibility Certification v4.0 in its accessibility criteria. Projects pursuing accessibility points should design and document to those standards from the outset.

Standardized multi-unit premium framework. CMHC introduced a revised premium structure for multi-unit financing in 2025, with a dedicated discount schedule for MLI Select based on points achieved and affordability commitments. Higher performance in affordability, energy, and accessibility translates to material premium reductions versus base multi-unit premiums.

MLI Select Eligibility: Who Qualifies

The program is broad in its eligibility, which is part of what makes it attractive to a wide range of investors.

Property requirements:

- Minimum of 5 rental units

- Eligible property types include apartment buildings, townhouses, mixed-use developments, and supportive housing

- New construction, substantial renovation, and refinancing of existing rental properties all qualify

Applicant requirements: Both individual investors and corporate entities can apply. The program was designed to be accessible to smaller investors, not just large development companies.

Geographic scope: MLI Select operates across Canada. Affordability calculations are always based on local median renter income, which means the thresholds differ by market. More on what that means for Atlantic Canada below.

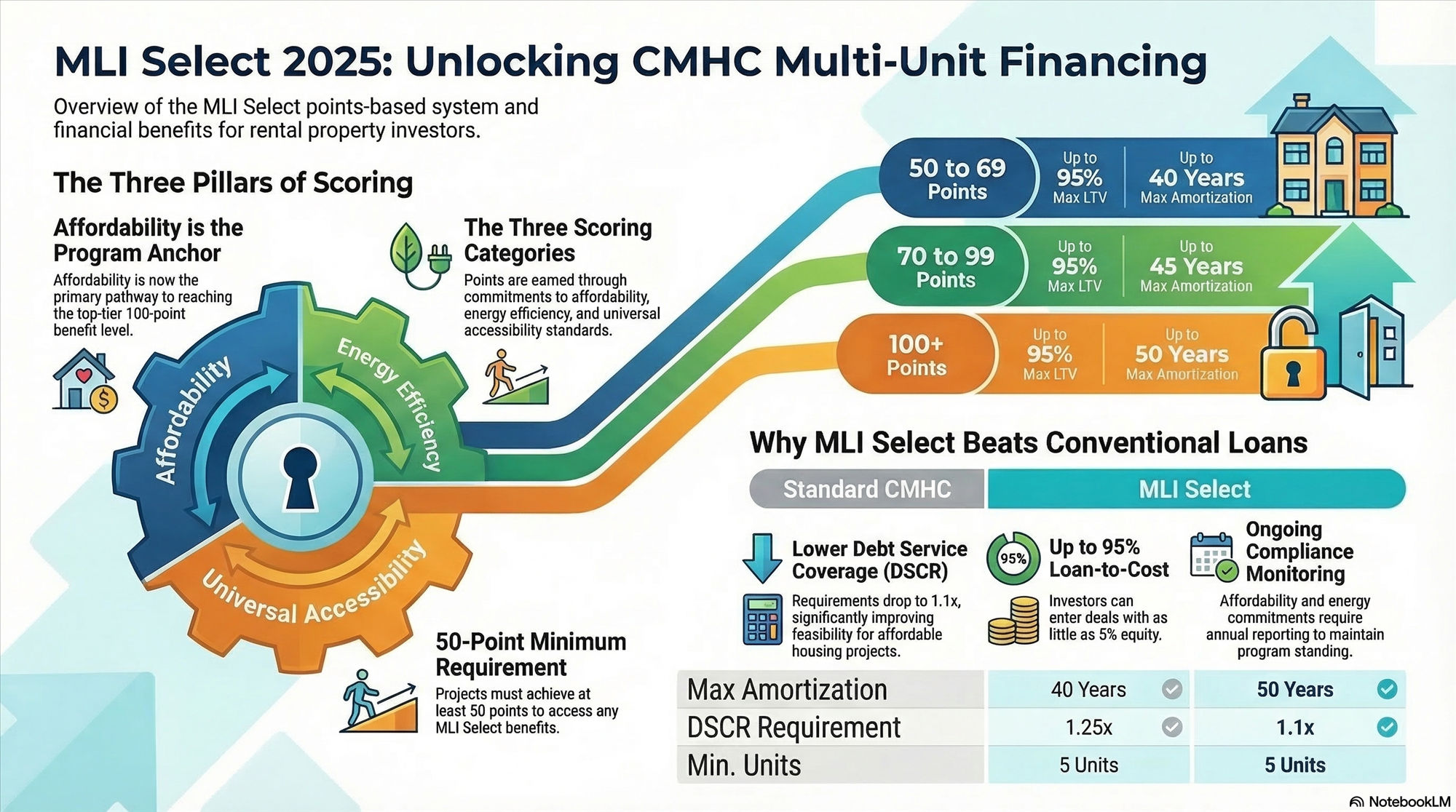

The MLI Select Points System: How Scoring Works

To access MLI Select financing benefits, your project must achieve a minimum of 50 points. Points are earned across three categories: affordability, energy efficiency, and accessibility. You can combine points from any mix of categories as long as you hit the threshold.

Affordability Points

Affordability points are earned by committing to rent a percentage of units at or below 30% of the local median renter income. Both the share of units and the length of the commitment affect your score.

Minimum commitment length is 10 years. Longer commitments (20 years or more) and higher percentages of affordable units earn more points.

Typical affordability targets (approximate bands):

| Affordability Commitment | Estimated Points |

|---|---|

| 40% of units at 30% of median renter income, 10 to 20 years | ~50 points |

| 50% of units at 30% of median renter income, 20 years | ~70 points |

| 60%+ of units at 30% of median renter income, 20+ years | ~90 to 100 points |

Note: CMHC publishes the full affordability points table. These ranges illustrate the general structure. Confirm current thresholds directly with CMHC or your lender.

Energy Efficiency Points

Energy efficiency points are awarded for exceeding baseline performance standards under the National Energy Code for Buildings (NECB). Qualifying measures include advanced insulation, high-efficiency HVAC systems, renewable energy integration, and smart building systems.

Energy efficiency can contribute meaningfully to your total score, but since the June 2024 revisions, energy alone is generally not a path to 100 points. Projects relying primarily on energy efficiency will typically land in the 50 to 70 point range unless affordability commitments are also included.

Accessibility Points

Accessibility points are earned by incorporating universal design features and meeting recognized accessibility standards. CMHC now explicitly aligns its accessibility criteria with CSA B651:23 and Rick Hansen Foundation Accessibility Certification v4.0. Projects pursuing these points should document compliance with those specific standards from the design stage forward.

Qualifying features include barrier-free entrances, accessible bathrooms, wider doorways, and adaptable unit layouts.

Strategic Point Optimization

The most efficient path to top-tier benefits is a project built around a strong affordability commitment, with energy and accessibility layered on top.

Important: After June 2024, affordability is effectively the anchor for reaching 100 points. A project built purely on energy efficiency or accessibility typically will not reach 100 points under the current framework. If you are targeting the highest benefit tier, your business plan needs to include a meaningful affordability commitment.

For projects where deep affordability is not feasible, a combined approach across all three categories, landing in the 50 to 70 point range, still delivers compelling financing improvements over conventional commercial mortgages.

MLI Select Benefit Tiers: What Your Points Actually Buy

This is where the points system translates into real dollars. Here is how the benefit tiers work:

| Points Achieved | Maximum LTV | Maximum Amortization | Notes |

|---|---|---|---|

| 50 to 69 points | Up to 95% | Up to 40 years | Base MLI Select benefits |

| 70 to 99 points | Up to 95% | Up to 45 years | Intermediate tier |

| 100+ points | Up to 95% | Up to 50 years | Top tier; limited recourse available |

LTV by asset type:

- New construction: up to 95% loan-to-cost/LTV depending on points achieved

- Existing properties: up to 85% to 95% LTV depending on points and program tier

The jump from 40 to 50 years of amortization has a significant impact on monthly payments and debt service coverage, which is why many developers run the numbers specifically to see what it costs to move from 50 to 70 or 70 to 100 points.

MLI Select Financing Benefits in Detail

High Loan-to-Value Ratios

Qualified projects can access up to 95% LTV financing. For many smaller investors, this is the most significant feature of the program. Rather than assembling 25% to 35% equity to enter a multi-family deal, MLI Select projects may require as little as 5%, freeing capital for additional projects or property improvements.

Investor callout: If you've been sitting on the sidelines of multi-family development because of equity requirements, MLI Select changes the math fundamentally. A 95% LTV on a qualifying project means your capital goes considerably further than under conventional commercial financing. [NEW LINK] Halifax's housing starts data for 2025 shows the rental segment is where the strongest development opportunity sits right now -- you can read the full breakdown here: Halifax Housing Starts in 2025: A Detailed Market Analysis and National Comparison

Extended Amortization Periods

Longer amortization means lower monthly payments, stronger cash flow during lease-up, and better debt service coverage ratios. As noted above, amortization ranges from 40 to 50 years depending on your point score.

The 55-year amortization you may have seen referenced in recent coverage applies in specific limited circumstances, not as a general feature of the program. Plan your proforma on 40 to 50 years.

Reduced Debt Service Coverage Requirements

Standard commercial mortgages typically require a DSCR of 1.25x or higher. MLI Select reduces this to 1.1x, which meaningfully improves feasibility for projects operating in the affordable rental segment where net operating income is constrained.

Reduced Insurance Premiums

Higher point scores unlock lower mortgage insurance premiums. CMHC's 2025 premium framework includes a formalized discount schedule for MLI Select, with material reductions available to top-tier affordability and energy/accessibility projects. The exact premium percentages shift periodically, so confirm current rates with CMHC, but the directional benefit is clear: higher scores mean lower premiums, compounding over a 40 to 50 year mortgage term.

MLI Select vs. Standard CMHC Multi-Unit Financing: A Quick Comparison

| Feature | Standard CMHC Multi-Unit | MLI Select |

|---|---|---|

| Maximum LTV | Up to 85% | Up to 95% |

| Maximum amortization | Up to 40 years | Up to 50 years (top tier) |

| DSCR requirement | Typically 1.25x | 1.1x |

| Insurance premium | Standard multi-unit rate | Discounted based on points |

| Social commitments | None required | Required (50+ points minimum) |

| Limited recourse | Not standard | Available at 100+ points |

If your project is earlier in its lifecycle and you are looking at construction-phase financing, the [NEW LINK] Apartment Construction Loan Program (ACLP) offers loans up to $55 million with flexible repayment terms up to 50 years and can be a complementary tool to MLI Select depending on how your deal is structured.

Quick Examples: What 50, 70, and 100 Points Look Like in Practice

Example A: 60-unit building, 50 to 70 points A developer commits 40% of units to rent at 30% of local median renter income for 20 years, and designs to basic CSA B651:23 accessibility standards. Result: approximately 70 points, 95% LTV, up to 45-year amortization, intermediate premium discount.

Example B: 120-unit building, 100+ points A developer commits 70% of units to rent at 30% of local median renter income for 20 years, combines this with a high-performance building envelope and HVAC system exceeding NECB baselines, and achieves RHF Accessibility Certification v4.0. Result: 100+ points, 95% LTV, up to 50-year amortization, top-tier premium discount, limited recourse potentially available.

These examples are illustrative. Your actual point score will depend on your specific commitments and CMHC's current scoring matrix.

Repayment Terms and Guarantee Structure

Guarantee Requirements

Construction and new development:

- 100% guarantee required during construction and lease-up phases

- Guarantee may reduce to 40% after rents have stabilized for 12 consecutive months

Existing property refinancing:

- 40% guarantee required, reflecting the lower risk profile of stabilized income-producing assets

Interest Rate Options

Both fixed and floating rate options are available, with preferential terms accessible at higher point scores. Choose the rate structure that fits your project's risk profile and hold period assumptions.

Monitoring, Compliance, and What Happens If You Fall Short

This section is missing from most MLI Select guides, and it matters to investors doing exit planning.

Affordability commitments under MLI Select are not just checked at application and forgotten. CMHC requires ongoing monitoring through annual compliance confirmations and rental roll reporting. You are expected to demonstrate that affordable units are being rented at committed rates, to eligible tenants, throughout the commitment period.

If commitments are not maintained, the consequences can include higher premiums, required reporting, or in more serious cases, forced refinancing under different terms. This is material to how you structure your ownership, management, and eventual exit from the asset.

Build your compliance monitoring into your property management processes from day one, not as an afterthought.

MLI Select in Atlantic Canada: What Nova Scotia Investors Should Know

Because affordability is always calculated based on local median renter income, the program works differently in Halifax, Dartmouth, Truro, and Colchester County than it does in Toronto or Vancouver.

In Atlantic Canada, median renter incomes are lower than in major urban centres, which means the dollar threshold for "30% of median renter income" is also lower. This can make hitting affordability point targets mechanically more achievable for developers who are already building or acquiring in markets where rents are more moderate.

For smaller projects in communities like Dartmouth, Truro, Stewiacke, or East Hants, the combination of a lower affordability threshold and the program's national eligibility scope means MLI Select is very much in play, even well outside the major metros.

The regulatory environment in Nova Scotia is also actively shifting in favour of development. [NEW LINK] The province recently created a dedicated planning department specifically to fast-track housing approvals in the Halifax Regional Municipality, reducing some of the approval delays that have historically slowed projects down: Nova Scotia Creates New Provincial Planning Department to Fast-Track Halifax Housing Development

In addition to MLI Select, Nova Scotia developers have access to a range of provincial, federal, and municipal funding programs that can stack alongside CMHC financing. [NEW LINK] For a full overview of what's available in this province, see: Your Complete Guide to Affordable Housing Funding in Nova Scotia

If you're planning a project within the Halifax Regional Municipality specifically, it's also worth understanding how the [NEW LINK] Suburban Housing Accelerator Plan is reshaping zoning and density rules across suburban Halifax, which directly affects where and what you can build.

Developer and investor callout: If you are planning a 5-plus unit project in Nova Scotia, I can help you model your points, run the pro forma, and assess realistic LTV and amortization options before you go to lenders. I work regularly with Nova Scotia investors, developers, and lenders who are actively doing MLI Select deals in this market. Connect with me here.

How to Apply for MLI Select: The Step-by-Step Process

Step 1: Project assessment Evaluate your project concept against all three scoring categories early, ideally before finalizing your design. Engage architects, engineers, and energy consultants who understand the NECB and CSA B651:23 standards.

Step 2: Points calculation Work with qualified professionals to project your expected score. Document everything that supports your claimed points.

Step 3: Pre-application consultation Use CMHC's pre-application consultation process. This is a valuable, underused resource that can surface issues before formal submission and save significant time.

Step 4: Document preparation Gather detailed project plans and specs, financial projections and operating pro formas, energy efficiency analysis and certifications, accessibility compliance documentation, and affordability commitment agreements.

Step 5: Formal submission Submit a complete package. Incomplete applications cause delays. CMHC underwriting evaluates both financial viability and program compliance.

Step 6: Closing and ongoing compliance After approval, complete mortgage documentation and set up your compliance monitoring system. MLI Select is a long-term commitment, and your management processes need to reflect that from the start.

Frequently Asked Questions

Can smaller investors access MLI Select? Yes. The program specifically aims to open multi-family investing to a broader market through reduced down payment requirements and lower DSCR thresholds.

Can I reach 100 points through energy efficiency alone? Generally not under the current framework. Since the June 2024 revisions, affordability is the primary pathway to 100 points. Energy and accessibility typically need to be combined with a meaningful affordability commitment to reach the top tier.

What if my project doesn't maintain its affordability commitments? You are subject to ongoing monitoring and reporting obligations. Non-compliance can result in higher premiums, additional reporting requirements, or forced refinancing. Build your compliance process into your property management from day one.

Does my project need to be in a major city? No. The program is national and applies to projects across Canada, including smaller communities. In Atlantic Canada, smaller centres like Dartmouth, Truro, and Colchester County all qualify if they meet points and underwriting standards.

What accessibility certification does CMHC recognize? CMHC now explicitly references CSA B651:23 and Rick Hansen Foundation Accessibility Certification v4.0. Design and document to those standards if you are pursuing accessibility points.

What is the 55-year amortization I keep reading about? The 55-year amortization is available in specific, limited circumstances, often related to default management or at-risk projects. It is not a standard offering for new development applicants. Plan your proforma on 40 to 50 years.

How does MLI Select compare to the ACLP? The two programs serve different purposes. [NEW LINK] The Apartment Construction Loan Program provides low-cost construction loans and is aimed at the development and building phase. MLI Select is a mortgage loan insurance product that applies to the longer-term permanent financing of completed or stabilized rental properties. Some projects may benefit from using both depending on their structure and stage.

Is MLI Select the Right Fit for Your Project?

The MLI Select program represents a genuine shift in how government-backed financing can support private sector housing development in Canada. For investors and developers willing to structure projects around affordability, energy performance, and accessibility commitments, the financing terms are among the most competitive available anywhere in the multi-family market.

The program rewards long-term thinking. Investors who treat MLI Select properties as long-term portfolio assets benefit most from the extended amortization, lower DSCR requirements, and premium discounts. If your strategy is a short flip, this likely is not your vehicle. If your strategy is stable long-term rental income with leverage that conventional lenders cannot match, it deserves serious attention.

[NEW LINK] The Halifax-Dartmouth market continues to show strong fundamentals for rental investment: Halifax Real Estate Market in 2025: Trends, Opportunities, and What Buyers and Sellers Need to Know

If you are planning a 5-plus unit project in Nova Scotia or Atlantic Canada, I can help you model your points, assess your pro forma, and connect you with lenders actively doing these deals. With over 25 years of experience in the Halifax and Dartmouth market, including a background as a licensed Home Inspector, I bring a different lens to how these projects actually come together on the ground. Reach out here.

Related Resources

- Canadian Bank Loans for Real Estate Development Are Surging -- Here's What's Behind the Boom

- Canada's Apartment Construction Loan Program (ACLP): Complete Guide

- Your Complete Guide to Affordable Housing Funding in Nova Scotia

- Halifax's Suburban Housing Accelerator Plan: A Complete Guide

- Halifax Housing Starts in 2025: A Detailed Market Analysis and National Comparison

- Nova Scotia Creates New Provincial Planning Department to Fast-Track Halifax Housing Development

- Halifax and Dartmouth Real Estate News and Market Reports

- Century 21 Optimum Realty -- Halifax Regional Municipality

Rob Lough is Broker/Owner at Century 21 Optimum Realty in Dartmouth, Nova Scotia. He has over 25 years of experience in residential and commercial real estate across the Halifax Regional Municipality, East Hants, and Truro markets, and holds a background as a licensed Home Inspector. He can be reached at (902) 880-8595 or Rob.lough@century21.ca.